{kind=link}

On March 25, Google Research published TurboQuant, a new AI compression algorithm that reduces the memory large language models need to operate by up to six times and boosts performance up to eight times, all through software, with no new hardware required. Within 24 hours, memory chip stocks around the world were in freefall.

The investor logic was simple: if AI suddenly needs six times less memory to run, then maybe the companies selling all that memory don’t have the growth story Wall Street had been betting on. Markets didn’t wait to think it through carefully. They sold first.

Micron was already in a rough patch before TurboQuant hit

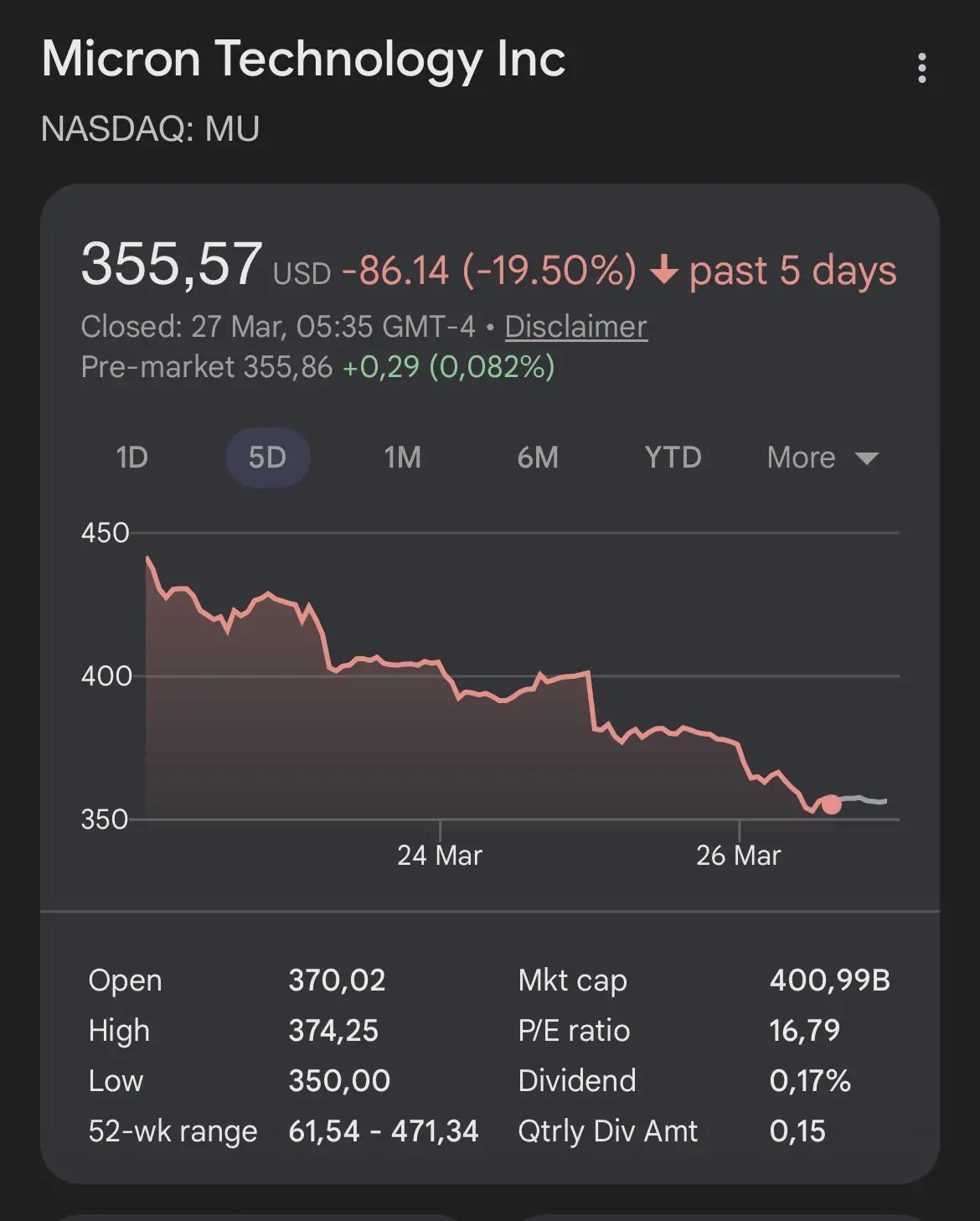

The timing couldn’t have been worse for Micron. Micron’s stock had already been declining for five consecutive trading days since March 18, dropping 17.2% from its recent high. This happened right after the company posted one of the most impressive earnings reports in its history, revenue of $23.86 billion, nearly triple the year prior, with earnings per share of $12.20 crushing analyst estimates.

So why was it falling? Peak-out concerns in the semiconductor sector had already been mounting since Micron’s earnings report. While absolute profit levels continue to grow, anxiety was centering on whether the rate of earnings growth had passed its peak.

Micron also announced a tender offer to buy back $5.4 billion of its senior notes that same week, a move that made some investors uncomfortable, raising questions about whether that was the right use of cash at this point in the cycle.

Then TurboQuant landed. After posting a smashing earnings report, Micron’s stock fell more than 20% across six consecutive trading sessions. The algorithm didn’t create the problem. It just made a bad week considerably worse.

Despite the stock sliding for a fifth day, retail sentiment around Micron on Stocktwits climbed to “extremely bullish,” with users pointing to a similar dip in December 2025 as a precedent for a rebound. Institutional investors and retail traders were clearly reading the situation very differently.

The numbers tell the full story of the damage

The sell-off moved in waves. It started in the U.S. on March 25 and rolled into Asia by the following morning. On the New York Stock Exchange, Micron Technology dropped 3.40%, SanDisk lost 3.50%, and Western Digital slipped 1.63%.

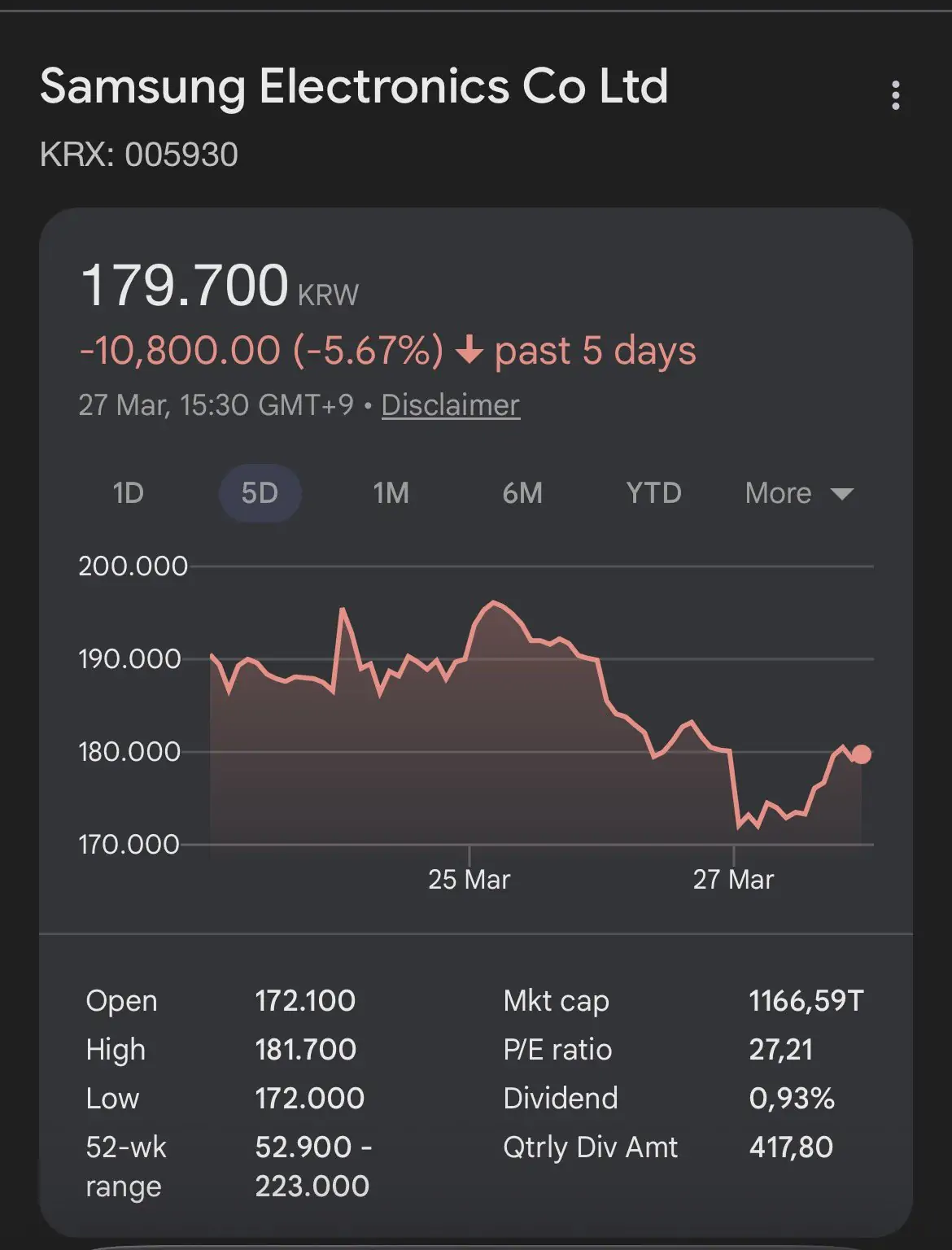

Asia took the harder hit. On March 26, the KOSPI index dropped more than 3%, with semiconductor names leading the sell-off. Samsung Electronics shares fell about 4.7%, while SK Hynix declined roughly 6.2%. Japanese flash memory company Kioxia dropped nearly 6%.

Foreign investors drove much of the Korean decline, selling large amounts of stocks even as individual investors were net buyers.

These aren’t small numbers for companies that had been on a historic run. Samsung shares had risen nearly 200% over the last year, while Micron and SK Hynix were each more than 300% higher. In two days, a significant chunk of those gains disappeared.

Analysts say the panic may be overdone

Most analysts aren’t buying the doom narrative. Ben Barringer, head of technology research at Quilter Cheviot, described TurboQuant as evolutionary, not revolutionary, saying it does not alter the industry’s long-term demand picture.

There’s also a technical argument the market may have missed. TurboQuant primarily optimizes VRAM during inference, not model weights, and its impact on high-bandwidth memory, which is crucial for AI training, is expected to be minimal. Training AI models, where the bulk of chip demand actually lives, is not affected by TurboQuant at all.

Wells Fargo argued the algorithm could actually end up being a positive for memory companies, making AI cheaper to run lowers costs, which tends to drive wider adoption and ultimately higher total demand over time. Morgan Stanley noted that lower AI operating costs could expand the overall market, and with the semiconductor sector’s 12-month forward P/E ratio at just 6.5 times, the prevailing view is that excessive panic should be avoided.

What this week really exposed is how fragile sentiment had become in the memory chip sector heading into earnings season. The stocks had tripled. Investors were already nervous. TurboQuant gave them a reason to act on that nervousness.

Whether the algorithm turns out to be a genuine long-term threat to chip demand or just a well-timed excuse to take profits, the chip giants are nursing real bruises, and the semiconductor world will be watching every data point closely from here.

Do you think this sell-off makes sense or is the market completely overreacting? Drop your take in the comments!